Why are premiums going up?

Rising healthcare costs and policy changes are making health insurance harder to afford. Learn what we can do together to fix it.

It’s making headlines and you see it in your bills: Healthcare costs are skyrocketing, and they’re driving up your insurance premiums and out-of-pocket costs.

What’s making health coverage difficult for businesses and employees and families and individuals to afford? And what can be done about it?

The answer to both: A lot.

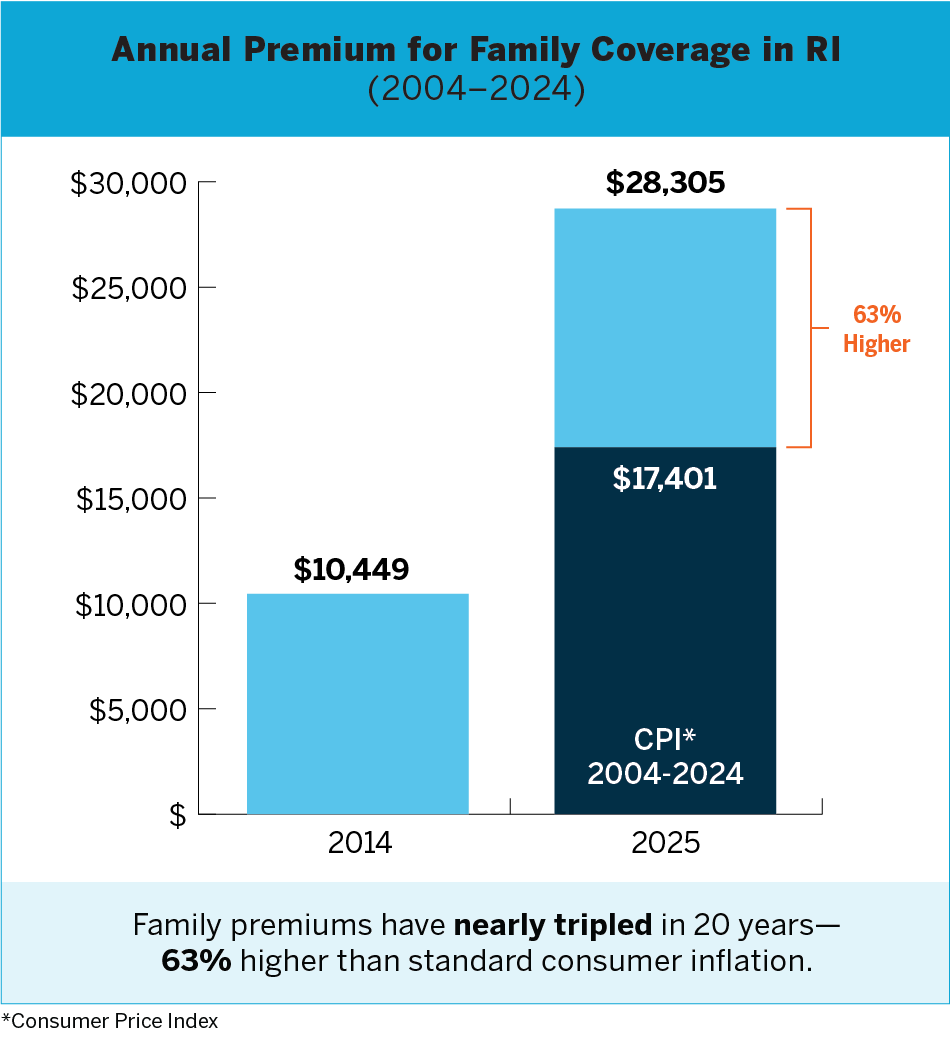

Numbers paint a troubling picture

As enrollment for 2026 health plans kick off, costs continue to rise at a rapid clip. According to a report by professional services company PwC, medical and drug claims paid by insurers are projected to climb next year by 8.5% for group insurance and 7.5% for individuals. That accelerated growth has persisted since 2024 and hasn’t been seen in 15 years. For comparison, the Consumer Price Index was 2.9% in 20241.

In Rhode Island, rising healthcare costs are driving up healthcare premiums, with some of largest increases occurring in the past couple of years. According to KFF Health News, the average cost of a family health insurance policy in Rhode Island climbed to $28,305 in 2024. That’s nearly triple what it was 20 years earlier—and 63% higher than the Consumer Price Index. For 2026, average premium increases ranging from 17.6% to 21% were approved for Rhode Island insurers by the Office of the Health Insurance Commissioner (OHIC).

What’s driving up healthcare costs?

Healthcare can be extremely complex. But one thing is simple: The dollars that insurers send out to pay for members’ care is paid for with dollars brought in through premiums. So when healthcare costs rise, premiums have to rise as well, further burdening individuals, families, and businesses.

In recent years, even those high premiums haven’t kept pace with the actual cost of healthcare. At Blue Cross & Blue Shield of Rhode Island (BCBSRI), medical and pharmacy costs have each increased 20% from 2022 to 2024, contributing to a loss of $115 million last year.

As prices climb—particularly for hospital services and prescription drugs—patients are receiving more care and more complex care. That trend began following the pandemic and hasn’t let up.

In 2024, BCBSRI saw costs continue to jump significantly. These include:

- 14% increase in pharmacy spending due in large part to high-priced specialty drugs for complex and rare health conditions as well as the rise of GLP-1 medications for diabetes

- 10% increase in outpatient care spending, including higher surgery costs and more ER visits

- 8% increase in inpatient hospital care spending, including higher hospital admission rates overall and shifts in where patients received care

In addition to growing healthcare service costs, KFF reported recently that insurers are highlighting policy changes as factors in rate increases, "including the expiration of the enhanced premium tax credits at the end of this year and the impact of tariffs on some drugs, medical equipment, and supplies."

For BCBSRI, regulatory changes, on both the local and national level, are adding to premium pressures across group and individual plans. These include:

State

- Primary care payments: In compliance with new OHIC requirements, BCBSRI payments to primary care providers increased 15% in July and will increase another 15% at the beginning of 2026.

- New premium assessment: A state law passed this year, which goes into effect in 2026, imposes a new assessment on all RI health plan premiums. Projected to raise $30 million, the revenues will be added to the state’s general fund for "primary care and other critical healthcare programs."

Federal

- New taxes/tariffs: These include new tariffs on imported pharmaceuticals, which are expected to further raise prescription drug costs.

- Expiration of enhanced premium tax credits: An Oct. 30 report by the Rhode Island Executive Office of Health and Human Services projects that the demise of the credits will, on average, more than double premiums for those losing them. The Peterson-KFF Health System Tracker notes that insurers expect "healthier enrollees to drop coverage. That, in turn, increases underlying premiums."

Already finding solutions

The best solutions to affordability are achieved through collaboration, and that trend is gaining encouraging momentum.

One of the most promising areas for insurers is improving care coordination through personalized service. One example at BCBSRI is a new cancer care support program with Daymark Health, created in close collaboration with providers to better support patients coping with the difficulties of cancer treatment. Daymark specialists complement the care of providers by helping members navigate the system and get more timely access to care. This rapid support can help improve members’ quality of life while also avoiding inconvenient and costly visits to an emergency room or doctor’s office. Although only several months into this partnership, BCBSRI is already hearing positive patient stories.

BCBSRI is also expanding programs that help members prevent disease and stay on top of chronic conditions. For example, BCBSRI is coordinating at-home care through HouseCall by Blue and putting powerful digital wellness tools directly into the hands of members, including ones designed specifically for women’s health and joint health.

To lower drug costs that are increasingly playing an outsized role in rising premiums, BCBSRI is pooling resources with insurers across the country. These efforts include group purchasing of high-cost specialty drugs, through Synergie Medical Collaborative2, and manufacturing low-cost generics and biosimilar medications, through Civica Rx3.

Premium relief can also come from insurer efficiencies. To lower administrative costs, BCBSRI has reduced staffing levels with a focus on management, consolidated vendor contracts, and deployed technology for greater efficiencies, contributing to nearly $20 million in savings for 2025. Federal law requires that insurers spend 80-85% of premiums on medical care or pay rebates, but BCBSRI, which serves members not shareholders, aims for 87% every year and actually spent more than 91% in 2024.

As a local, tax-paying nonprofit, BCBSRI remains committed to working with elected officials, healthcare leaders and the provider community on these efforts. Together, we can advance solutions to keep premiums affordable, recognize that unfunded government mandates can drive premiums up, and put the brakes on runaway healthcare costs.

Follow Today’s Healthcare Costs as we continue to explore what’s driving up healthcare costs and how BCBSRI is addressing affordability for our members.

1Consumer Price Index: 2024 in review : The Economics Daily: U.S. Bureau of Labor Statistics

2Synergie Medication Collective℠ is an independent entity owned by the Blue Cross Blue Shield Association and individual Blue Cross and Blue Shield companies. Civica Rx is an independent company partnering with Blue Cross & Blue Shield of Rhode Island and other Blue Cross and Blue Shield companies to provide select generic drugs to members.

3Civica Rx is an independent company partnering with Blue Cross & Blue Shield of Rhode Island and other Blue Cross and Blue Shield companies to provide select generic drugs to members.